Credit card marketing used to be a straightforward path. Today’s journey is more like a maze. Cardholders need convincing to choose your card, activate it, make their first purchase, and use it regularly to gain the most benefit.

But there are many challenges along the way:

- Consumers have so many options to choose from that they suffer from information overload.

- Activating cards today requires more hoops and jumps.

- Consumers are spending more time on digital channels, making traditional tactics like direct mail less effective.

- Competition is fierce and new card issuers have blurred the lines between banks and fintechs.

The big takeaway: card issuers must find a way to engage consumers as part of the entire credit card journey.

Instead of pushing customers through a funnel using traditional methods, issuers should guide customers with an engaging and immersive digital experience. And gamification is the best way to achieve this. 🎮🃏

Today, we’re your guide to this new cardholder experience. So keep reading for a breakdown of how gamification powers every stage of the cardholder lifecycle.

When does gamification make sense across the cardholder lifecycle?

Cardholders want their experience to be simple, easy, and rewarding. They want perks and benefits to make their life easier. So, now is the moment to take a more rewarding marketing approach.

Issuers that integrate gamification have the upper hand when it comes to challenges such as savvy competitors. And it’s clear that early adopters will lay the foundation for enhanced cardholder experiences.

With this in mind, let’s take a look at how gamification can power the entire cardholder lifecycle.

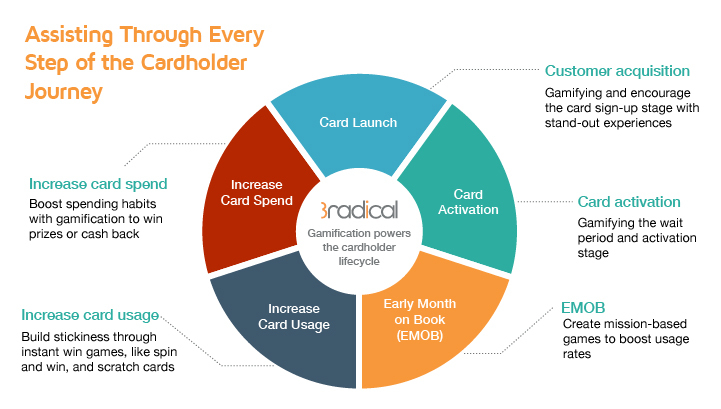

Card launch/customer acquisition

The cardholder journey starts when a card issuer launches a new card product or a new acquisition campaign. Either way, card issuers will need an effective approach to capture new customers.

Key challenge

At the acquisition stage, customers have a vast choice of card issuers to choose from. Which means card issuers have to stand out from the crowd.

Solution

This is where the card issuer can distinguish their brand amongst a sea of competitors through an engaging experience.

Gamification example:

- Gamify the card sign-up stage: Introduce a point-based game whereby completed user actions will earn chances to instantly win prizes through mini-games, like spin-the-wheel.

It’s even better if you can use gamification to leverage zero-party insights, such as consumer preferences, reasons for choosing your card, competitor insights, and more.

Card Activation

At the card activation stage, cardholders often need prompting to activate their card. In fact, according to The Nilson Report, the average credit card activation rate for the top 50 Visa and Mastercard issuers is 57%. This leaves just over half of your acquired customers unactivated and unused – representing a lost opportunity, as well as wasted marketing resources in customer acquisition.

Key challenge

Card issuers struggle to reinforce their credit card value proposition and maintain cardholder excitement during the waiting period after acquisition, leading to low activation rates.

Solution

This is where gamification can really help to entice and reward customers for activating their card.

Gamification example:

- Gamify the waiting period. For each additional day a customer has to wait for a card, the chances that they will activate it decrease. Issuers can reduce the impact of this waiting period by making the card traceable in the mail, like an Amazon purchase, which gamifies the process and creates anticipation for the card’s arrival.

Early Month On Book (EMOB)

The period after acquisition is high stakes for card issuers. Their behaviours during their first 60-90 days with the card set usage patterns that will last the lifetime of the relationship, for better or for worse. According to the same above report, customers who receive EMOB messaging have three times the lifetime value of other customers, but card issuers generally under-invest in this vital stage.

Key challenge

A key challenge to this strategy is the ability to motivate newly-acquired cardholders to start – and continue – to use the card (more on this next). Unfortunately, most issuers lack the tools to effectively influence customer behaviour during these key stages of the cardholder lifecycle.

Solution

Personalised offers and experiences can boost usage rates and set profitable spending habits during EMOB, increasing lifetime value. Campaigns will create a value exchange for customers instead of simply demanding their attention.

Gamification example:

- Mission-based game that takes customers through chapters, earning them badges upon each chapter completion.

Increasing card usage

In recent years, some card issuers have changed their focus from simply acquiring new customers to optimising relationships with existing cardholders. Optimising usage will deliver huge impacts on customer lifetime value (CLV) as this is the stage where the issuer generally recoups acquisition costs and generates revenue.

Key challenge

Encouraging card usage and ‘stickiness’ can be challenging in a world of payment options. Why should they use your card over a different payment method?

Solution

Gamification can build loyalty and stickiness at a relatively low cost compared to other tactics. By providing value beyond the transaction, issuers create a value exchange that builds trust with the customer, who comes to feel that the issuer knows them and their needs.

Gamification example:

- Spin-to-win type campaign whereby X number of card transactions will trigger chances to play a game to win prizes or cash back.

Increasing card spend

Finally, when a customer is fully onboarded and credit card usage is happening on a regular basis, issuers enjoy steady revenue, especially if the customer has set profitable card habits. Card issuers that leverage gamification to engage customers regularly at this stage can see a significant impact on CLV.

Key challenge

Encouraging card spend often relies on running high-volume campaigns with low conversion rates. Traditional reward programmes are stagnant. Today, simply having a rewards program is not enough to encourage redemption.

Solution

Drawing on gamification can significantly boost card spending habits.

Gamification example:

- Spin-to-win type campaign whereby a certain value of transactions or spending tiers will trigger chances to play a game to win prizes or cash back.

Create more value across the cardholder experience with 3radical

Card lifecycle marketing using traditional techniques is no easy task. It can be near impossible to engage today’s digital consumers. Instead, it calls for new kinds of tools. We need to provide cardholders with an immersive digital experience, not siloed offline direct mail.

In short, card issuers need to re-imagine a cardholder lifecycle strategy that is engaging, rewarding, and fun. By boosting activation rates and proactively encouraging spending behaviours early on, issuers set themselves up for success at the usage stage and beyond.

3radical’s gamification approach taps into design thinking, actionable insights, and iterative testing. By providing meaningful, relevant experiences, issuers can reduce costs, and enable personalisation that, in turn, drives customer engagement and builds trust.

These elements work together to enhance the cardholder journey and deliver sustainable business growth.

👉Keen to find out more about Gamification? You can view a quick overview here.

Or you can find out more about our Quickstart package here. Or simply contact us today.